If you’ve recently renewed your car insurance policy, you’ve probably noticed the significant rise in prices over the past 18 months.

This hike in premium costs has been almost indiscriminate, affecting both new and experienced drivers across all types of vehicles, and all levels of cover.

Here we explore the facts behind the rise in motor renewal prices, including some of the key factors exacerbating claims inflation, and how insurers are acting to mitigate their effect.

How much have insurance premiums increased?

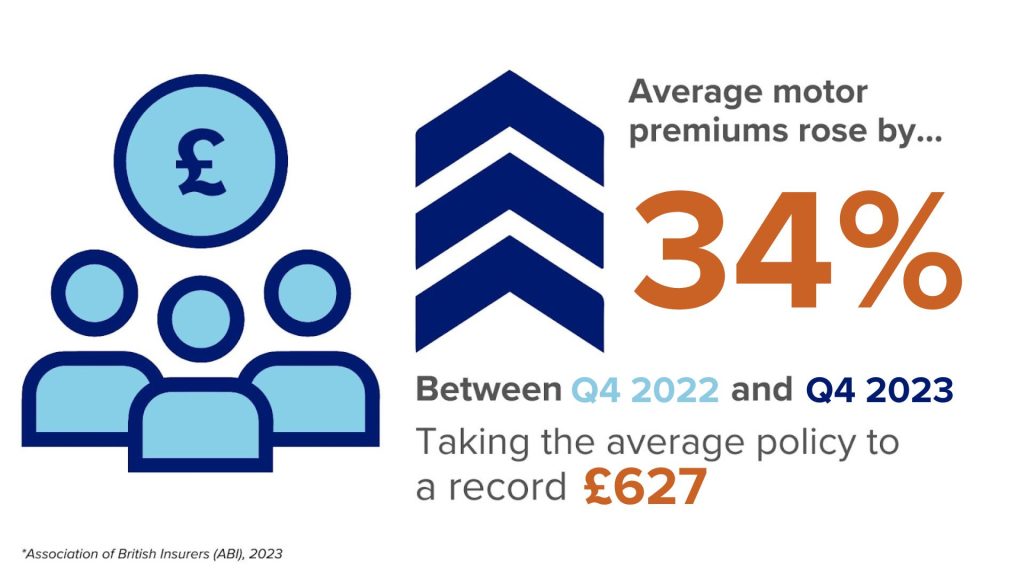

According to data from the Association of British Insurers (ABI), insurance premiums rose by an average of 34% between Q4 2022 and Q4 2023.

This took average renewal costs to a record high, standing at £627 in December 2023, compared to just £471 in Q4 2022.

As a result, the average driver is now paying almost £160 more to insure their car than they were a year ago, exacerbating the ongoing cost of living challenges.

Why is car insurance getting more expensive?

Renewal prices are rising due to a significant increase in the cost of insurance claims.

Inflationary pressures are making it more expensive to repair or replace customers’ vehicles if they’re involved in an incident, increasing costs to insurers, and pushing up the price of premiums for their customers.

Here are some of the key factors fuelling this hike in vehicle repair & replacement costs, and ultimately leading to higher renewal prices…

1 – Increased operational costs for repairers

As with all businesses, general inflation is leading to higher operating costs for vehicle repairers, particularly when it comes to energy bills and recruitment costs. This is forcing them to increase their prices and rates in-line with inflation to mitigate financial risk to their businesses.

This means insurers are paying more on average to have customers’ vehicles repaired when they’re involved in an incident, pushing up the total cost of claims, thus hiking premium prices.

2 – A shortage of repair slots & bodyshop capacity

During the COVID-19 pandemic, a lack of work meant many vehicle repair shops were forced to close their doors for good. The industry is yet to recover from this decline in service coverage, meaning demand for vehicle repair far outweighs available capacity in many regions.

This means it often takes longer for insurers to find appropriate repairers with capacity to repair their customers’ vehicles, pushing up the cost of things like vehicle storage and courtesy car hire. In fact, the ABI reports that insurers spent an astonishing 47% more on courtesy vehicles in Q3 2023, compared with the same period in 2022.

3 – Difficulty sourcing cost-effective replacement parts

International supply chain challenges are making it harder for repairers to source replacement parts for customers’ vehicles. This is especially true for newer vehicles, which often require brand-new parts to be shipped directly from the manufacturer, due to a lack of aftermarket or second-hand alternatives.

It also means repairers are granted fewer purchase options when sourcing replacement parts, leaving them unable to source the discounts they’re used to, and thus paying higher prices.

This, combined with the lengthened delivery times for high-demand components, is leading to further delays and added costs, which are passed onto insurers and their customers.

4 – Inflation in the value of both new & used cars

The value of both new and used vehicles has been increasing, with AutoTrader’s Retail Price Index revealing that second-hand car prices have soared by almost 20% since 2021.

This has been primarily fuelled by a shortage of semiconductors, which many new vehicles use to power their computer systems. This has delayed production of new cars dramatically for many manufacturers, and pushed consumer demand towards used vehicles.

Higher vehicle value means it costs more to replace them if they’re damaged beyond repair, drastically inflating the payout cost of ‘total loss’ claims for insurers, and consequently increasing premiums.

It also means there’s a higher threshold for declaring cost-based write-offs, as the increased value of the car makes it preferable to conduct even extensive repairs rather than paying for a replacement. This further exacerbates cost control challenges for insurers, making it difficult to minimise the financial impact of more complex claims.

5 – The increase of EVs & complex vehicle technologies

The technology present on modern cars is becoming increasingly complex, presenting repair challenges and often added costs when they need repairing.

Vehicles with electric/hybrid powertrains, or onboard safety features like ADAS, require specialist attention if they’re involved in an incident. This means insurers are often required to pay higher repair rates, or cover additional services like ADAS recalibration, which inflate the total cost of claims.

With EV and hybrid adoption fast accelerating, insurers are seeing higher claims costs across the board – leading to more upwards pressure on insurance premiums.

What are insurers doing to combat rising costs?

Despite the multifaceted nature of premium inflation, insurers are taking action to reduce the impact of market challenges on their customers, and bring down the cost of claims.

Here are some of the steps the industry is taking to mitigate the increasing cost of vehicle repair, and the obstacles they’re facing throughout the process.

Harnessing alternative repair methods, and ‘repair over replace’

In an effort to counter both delays and rising repair rates, insurers have been increasing their use of alternative repair methodologies like mobile SMART repair.

These methods prioritise ‘repair over replace’, conducting high-quality, targeted repairs to damaged panels without the need to replace them entirely.

This helps to reduce both the cost and turnaround of repairs, and can even be delivered by mobile technicians at the customer’s home – reducing reliance on high-demand bodyshop capacity.

Read More: Plastic Bumper SMART Repair to suit ‘Repair Over Replace’ Methodology

Sourcing more green & aftermarket parts

As well as harnessing ‘repair over replace’ methodologies, insurers have been diversifying their parts sourcing strategies to include more green & aftermarket alternatives.

Second-hand or off-label parts are often cheaper to purchase, provide quicker turnaround, and can deliver exactly the same quality you’d expect from a new OE component.

This helps insurers to counter some of the rising costs throughout the repair process, as well as counter the current delays to international manufacturing and shipping, without compromising on quality or safety.

Enhancing their approach to repair engineering, and cost control

Controlling repair costs is at the core of most insurers’ risk management strategies, prompting them to increase their focus on engineering swift, cost-effective repairs.

Insurers are working with their accident management partners to develop more intelligent engineering solutions, which help them to identify opportunities for cost-saving measures like repair over replace or green parts.

Engineers look at estimates provided by repairers to ensure the parts and methods suggested provide best value, quality, and turnaround. If they find a more accessible or cost-effective solution, engineers can suggest this to repairers on a case-by-case basis.

This tailored approach allows them to easily save time and money on more straightforward repairs, while also enhancing cost control for vehicles with more extensive requirements.

Effective engineering can help to reduce the number of vehicles written off for cost-related purposes, minimise the cost of replacement parts, and ultimately reduce claims costs across the board.

Expanding the capacity & capability of their repair networks

Insurers are taking action to expand the reach, capacity, and capability of their repair networks. This has included partnering with a wider range of repair specialists, including those with EV & ADAS expertise, and harnessing on-demand repair capacity to cope with increased demand.

This helps them to speed up repair turnaround for customers, without relying on high cost out-of-network providers, ultimately helping to reduce the costs of claims, and bring premium prices down.

What is Activate Group doing to support them?

Here at Activate Group, we work with our insurance partners to understand their unique cost control challenges, and develop new solutions & innovations to mitigate them.

Here are some of the actions we’re taking to help our customers reduce the cost of claims…

In-house engineering & repair cost control

Our in-house engineering team helps insurers to reduce the cost and turnaround of repairs. Our engineers look at each claim on an individual basis to ensure repairs are conducted using best-practice methods, and the most cost-effective parts & methodologies.

Using the estimates provided by repairers, our engineers work to identify opportunities to save time and money throughout the repair process. This often includes suggesting alternative sources for replacement parts, like aftermarket or ‘green’ supply chains, and utilising time-saving techniques like mobile/SMART repair.

Self-owned EV & ADAS-capable repair centres

We’ve invested in a network of self-owned repair centres across the UK, each with the tools and technologies to accommodate all vehicle types, including EVs & hybrids. Our Activate Accident Repair bodyshops are located in the areas our customers need them most, helping them to overcome regional demand, and facilitate quicker deployment & turnaround.

In-house parts supplier & aggregator

Our repair network is supported by our in-house parts aggregator, Activate Parts, which provides our customers access to at-purchase discounts and quicker delivery on replacement components. Through our diverse supplier and manufacturer relationships, we can source everything from new OE to ‘green’ parts, using live industry data to identify which provides the best cost & turnaround for each repair.

Harnessing industry data to mitigate obstacles proactively

We’ve been increasing our partnerships with industry leaders in automotive data & market analysis, allowing us to identify potential cost & demand challenges ahead of time, and take action to mitigate them proactively. We use these insights alongside our in-house claims data to ensure our customers are always prepared for periods of surge, supply/demand challenges, and fluctuation in parts/repair costs.

On-demand repair management with Repair-as-a-Service

Our Repair-as-a-Service solution allows insurers to access our repair management expertise on-demand, with no existing contract required, or long-term volume commitments.

This includes direct, on-demand deployment of repairs into our purpose-built bodyshops, as well as the option to utilise triage, engineering, and repair management if required.

This helps insurers to tackle repair demand strategically, reducing the risk of backlog within their own network, which leads to delays for customers, and added claims costs.

Learn more about our Repair-as-a-Service solution, and how it can help insurers to overcome their repair capacity challenges, improving outcomes for their customers:

In Summary

Car insurance premium prices have been on the rise over the past 12 months. Data from the Association of British Insurers shows the average premium rose by a staggering 34% between Q4 2022 and Q4 2023.

This rise has been fuelled by an increase in the cost of claims for insurers, fuelled by inflating costs and industry challenges within vehicle repair and manufacturing.

Some of the key factors pushing up motor claims costs include…

- Inflation leading to higher operational costs for repairers & bodyshops

- A post-pandemic shortage of repair slots & bodyshop capacity

- Challenges with international vehicle parts manufacturing & shipping

- Inflation in the value & retail price of both new and used vehicles

- The increased complexity of vehicle technology provoking higher repair rates

Despite the multifaceted nature of claims inflation, insurers are taking action to combat some of the rising costs, and reduce the impact on their customers’ premium prices, including:

- Harnessing alternative repair methods, like mobile & SMART, to save time and cut costs

- Sourcing more green & aftermarket parts to mitigate supply chain issues

- Enhancing their approach to repair engineering & cost control

- Partnering with more EV & ADAS-capable repairers to accommodate emerging vehicle technologies